We’re sure you’re thinking, “Wait, how can Illinois run out of insurance?” The answer is not a simple one, as it involves several different economic factors whose untimely overlap has caused unprecedented disruption in the insurance industry. We’ll do our best to break down this complex situation so you can understand any changes you may be seeing in your own policies.

Reduced reinsurance is driving changes across the industry. Insurance companies rely on larger, reinsurance companies to back their claim payouts in the case of catastrophic weather events. Unfortunately, this year reinsurance companies have severely limited the amount they’re willing to offer insurance companies to cover their claims, leaving them over-exposed in the event of a disaster.

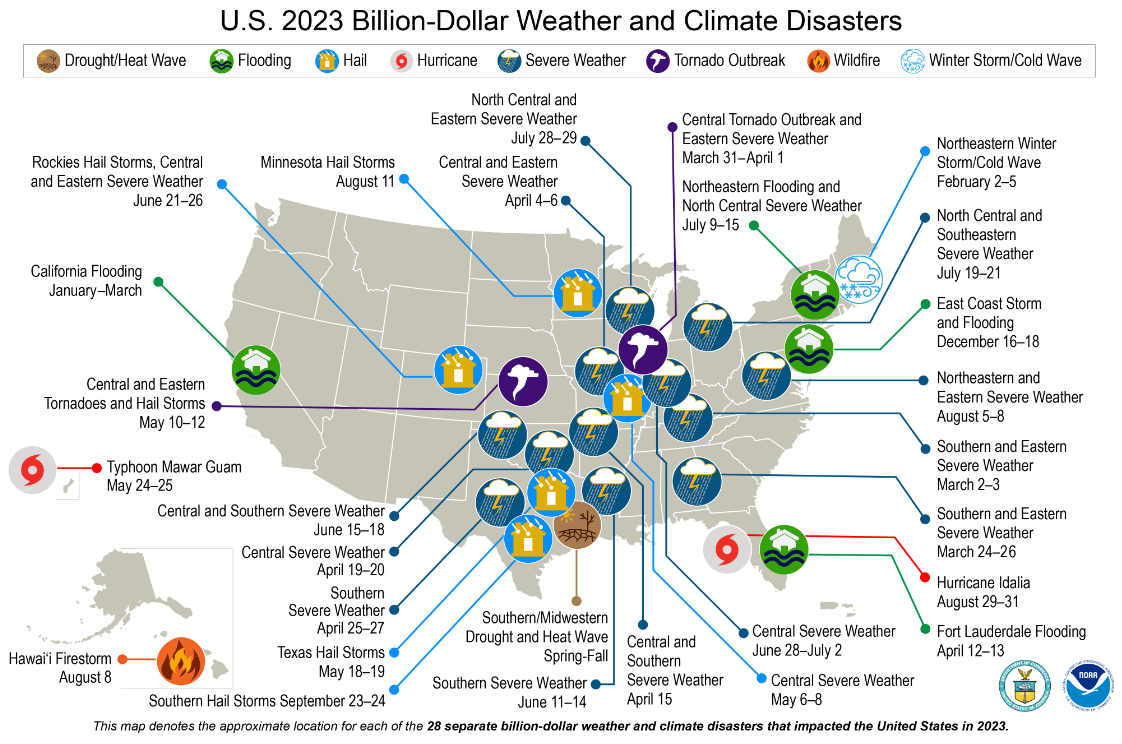

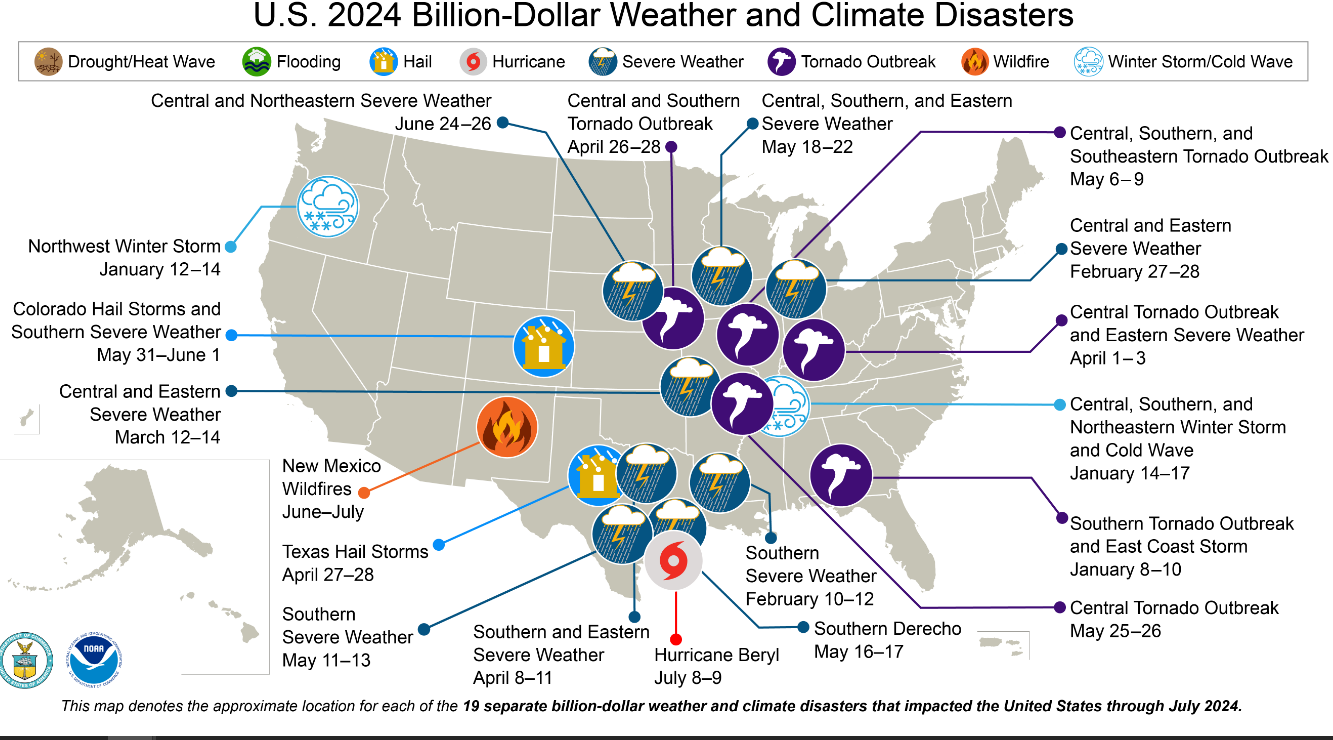

And those disasters have been happening with increasing frequency lately. Even excluding the major hurricanes in the East and wildfires in the West, we have seen a huge increase in smaller “convective storms,” including tornadoes, derechos, straight-line winds, hail and even lightning, especially in the Midwest. Data from the National Oceanic and Atmospheric Administration shows that from 1980 to 2005, the US saw just 2 to 4 severe convective storms per year that produced losses of $1 billion or more. During the last 6 years, that number has jumped to 18 such events annually, on average.1 And in just the first 9 months of 2023, we have had 23 extreme weather events nationally that cost at least $1 billion, totaling more than $57.6 billion in damage.2

The increased volatility in the weather, combined with worldwide economic policies, has resulted in fewer venture capitalists placing their investments with reinsurance companies. But the need for reinsurance coverage has only gone up as catastrophic storms have become more frequent. As the surging demand has collided with the diminished supply of available reinsurance, steep rate increases in reinsurance premiums and higher deductibles for insurance companies have followed.

As a result, insurance companies are now paying higher reinsurance premiums and are responsible to pay out significantly more catastrophic claim dollars each year. It is not an exaggeration to say that insurance companies have never seen anything like this, and it has shaken the industry to its core.

Insurance companies are being forced to make dramatic changes to how they do business. The sudden and unexpected contraction of the reinsurance market has left insurance companies feeling over-exposed. As a result, many insurance companies have made similarly sudden and unexpected changes to their own business guidelines. We have entered what’s called a “hard market,” in which insurance companies become so restrictive that it becomes genuinely “hard” to buy insurance.

Some examples: almost of all of our companies have had to become more selective in who they’re willing to insure, and many have had to pause accepting new customers altogether as they attempt to deal with the dual events of increased catastrophic claims and reduced reinsurance coverage to pay for them. Customers are also having to share more in the cost of their claims in the form of higher deductibles. Claim coverages are changing, as most companies transition to covering roofs at their current values at certain ages, rather than at full replacement cost. And of course premiums are rising by eye-popping amounts, as increased catastrophic losses drive increases in rate.

Widespread advice from many of our companies is that if you currently have insurance coverage, keep it. If you need new insurance, be prepared for a potential uphill battle to find the coverage you need. We here at Tomco will always strive to help you find the most competitive coverage at the most competitive cost, but be aware that if you’re searching for new coverage, your available choices may be limited for the foreseeable future.

What are we doing at Tomco to help you weather this storm? We know the current hard market is challenging (believe us, we know), and we want you to know we’re doing everything we can to help you get through it.

As new updates are announced, we are constantly evaluating the changing coverages and premiums and comparing them to our available options. We continue to partner with multiple companies to ensure we have the largest number of options possible, and we are continually looking for alternative coverages or policies that might serve you better. Our goal is to be proactively searching for and reaching out to you with options if we find them, so you can rest assured that the policies you have are your best option at this time.

Please don’t hesitate to contact us if you have questions, and know that even with our increasingly limited options, we are committed to giving our very best effort to find the coverages that work for you. Illinois hasn’t quite run out of insurance yet, and it is our hope that the extreme conditions we’re seeing in the industry will ease sooner rather than later. Until then, we encourage you to practice your patience and reach out to us with your questions. Together, we will make it through this.

1 Insurance Journal, “Is Industry Prepared? Hail, Convective Storms, Population Now Driving Billions in Losses,” October 4, 2023

2 Insurance Journal, “US Already Sets Record for Yearly Billion-Dollar Weather Disasters,” September 13, 2023

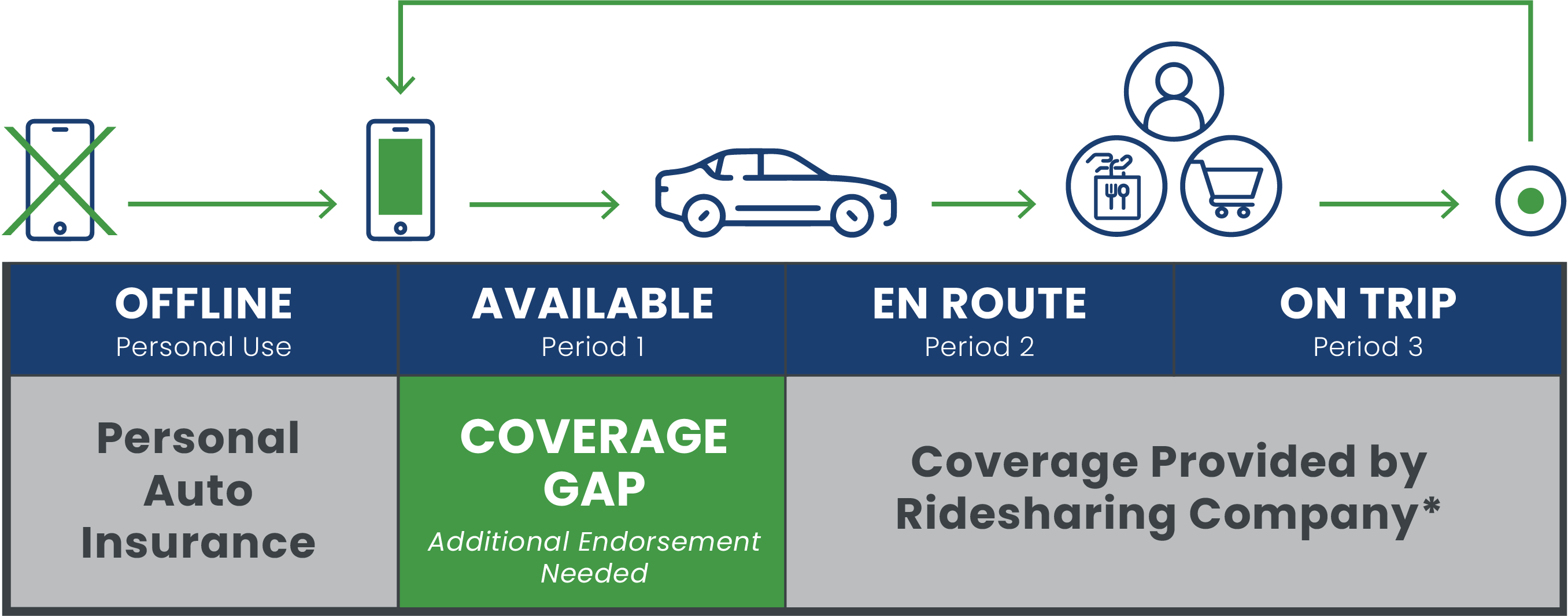

*We recommend you confirm coverage with your TNC.

*We recommend you confirm coverage with your TNC.

We’re happy (and sad) to announce Clarence's retirement on June 1st, 2022, after 48 outstanding years.

We’re happy (and sad) to announce Clarence's retirement on June 1st, 2022, after 48 outstanding years.